Audit Report 2022

320 Billion Cash Loss

By Mohamed Konneh

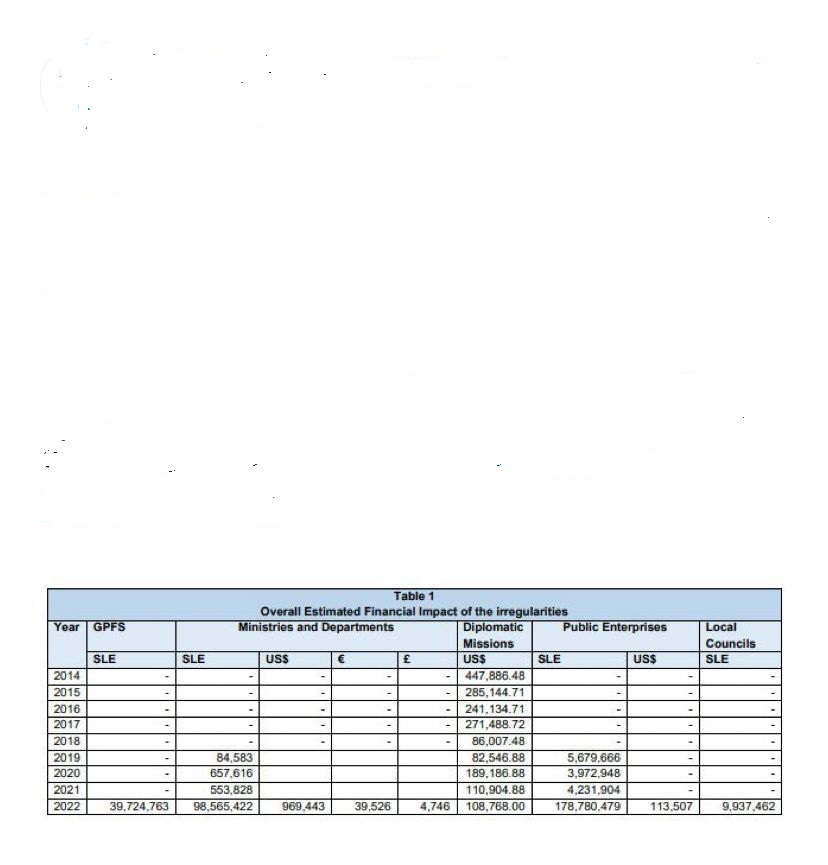

The 2022 Auditor General’s report has reported a cash loss of 320 Billion old Leone and 1.1M USD in the GPFS, MDAs, Diplomatic Mission, Local Council and Public Enterprises. The cash loss is accumulation from previous audit on a number of unresolved issues.

The report presents a comprehensive analysis of the findings, recommendations, and conclusions obtained from conducting financial, compliance, performance and information systems audits in Ministries, Departments and Agencies (MDAs).

The 2022 auditor General’s report embarked on a total of 108 audits: 32 Ministries and Departments, 45 Public Enterprises and Commissions, 22 Local Councils, six Diplomatic Missions and three Performance audits.

The report also contains irregularities with financial impact that brings to the attention of Parliament in accordance with 95(1) of the Public Financial Management Act, 2016.

In the statement of the Auditor General, Abdul Aziz Bangura stated thus ‘by our professional judgement, we established to a reasonable level that public monies were used by government in the manner intended by parliament. We assessed how they were used in terms of economy, efficiency and effectiveness. We also report to the citizens through parliament, how these activities were implemented.

In the area of irregularities the report stated that irregularities are acts of omission or commission by MDAs, contrary to the public financial management laws and regulations, contract agreements, and other applicable statutory instruments that were in existence during the audit scope.

Irregularities were classified within the public financial management system under the following categories: imprest not retired, statutory deductions not paid, assets and stores management, payments/expenditure management, salary and payroll management, procurements and contracts management and revenue management.

Notwithstanding the encouraging steps employed by the NRA to improve the revenue generation performance, the 2022 report noted some gaps in the revenue assessment, collection, and reporting.

These gaps could be attributed mainly to the failure of the NRA to collect tax revenue and apply penalties and sanctions against defaulters.

Input GST Wrongly Claimed by Taxpayers not supported Section 29(5a) of the GST Act of 2009 requires the submission of supporting documents before a tax credit GST can be claimed.

The report however, noted that input GSTs totalling SLE39,724,763 were not supported by relevant documentation, such as the schedule of local purchases and import GST in the Integrated Tax Administration System (ITAS).

Revenue not Traced to the Consolidated Fund and that the transit banks expected to transfer the revenue collected into the consolidated fund account at the Bank of Sierra Leone (BSL) within 24 hours upon receipt did not do so. The Sierra Leone Commercial Bank made a transfer totalling SLE3,565,919 regarding income tax revenue collected during 2022 to the BSL. The report stated thus noting they could not trace this transfer in the Income Tax accounts held at the BSL.

The Audit Service Sierra Leone (ASSL) has continuously improved on its efficiency and effectiveness of the audit process, to ensure that the results of audit and the recommendations thereof are credible, relevant, reliable and value adding. This is geared towards influencing improved decision making and positive impact on the livelihood of citizens. Provision of quality and effective audit services and confirmation of the compliance and effectiveness in programme implementation requires comprehensive scrutiny and evaluation of supporting documents.

.jpeg)